The State Of Retail Payments In Middle East And Africa

Service providers are introducing new payments infrastructure in Middle East and Africa

In this part of the changing global payments series, I am showcasing how technology has enabled digital payments infrastructure for the first time in many parts of the Middle East and Africa region. At the same time, as consumer expectations continue to change, regulation is also starting to kick in to offer a supporting role to some of the newer market entrants and innovations.

Of the 1.6 billion individuals lacking access to financial services globally, over 700 million are found in the Middle East and Africa (MEA) region. This serves as an incentive for many governments in the region to review and update regulatory frameworks as part of efforts to extend banking services.

In turn, this is paving the way for alternative providers such as mobile network operators and remittance companies, which are increasingly being recognised as regulated financial providers. It must be stated though, that innovation is moving faster than regulation and much still has to be done regulation-wise so as not to stifle the next phase.

The key technology in the region is mobile phones, which are ubiquitous and, in some countries, serve as an infrastructure to not only extend financial services but to introduce services for the first time to the unbanked, leapfrogging traditional banking services. While mobile payments/wallets are gaining traction globally, it should be remembered that such payment methods are not reliant on smartphones and that even basic phones can be used to make payments.

The number of the unbanked population has dramatically reduced since the introduction of mobiles to the payments infrastructure, which ushered in a new era of financial services to the market thanks to the fact more people have access to mobiles than bank accounts.

SMS

In certain parts of the MEA region, consumers use the very basic technology of text messages (SMS) sent from mobile phones as a way to pay for goods or services. One benefit of such a model is that it serves as a cheap and alternative method of payment acceptance and receipt for some micro and small businesses. Furthermore, it is generally secure, as no personal details or account details are released.

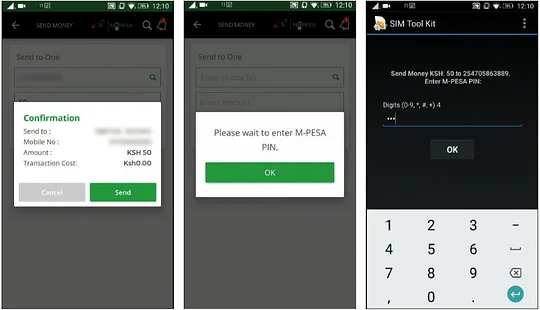

M-Pesa

M-Pesa stands as one of the widely known mobile money platforms, allowing users to store and move money. It was launched in Kenya in 2007 by telecoms provider Safaricom to address the lack of financial access in a country where mobiles were easier to access than banking services. Only 19 percent of the population had access to banking and electronic payment services before M-Pesa came on the scene and by the end of 2018, the number had risen to 83 percent. With over 30 million active users in the country, M-Pesa has been critical in providing consumers with an alternative payment method to cash.

Understanding the challenges faced by the local consumers, such as internet connectivity, accessibility and affordability, M-Pesa’s infrastructure was designed to be compatible with all types of mobile phones.

Users register for an account using agents usually located in grocery stores or fuel stations. The user’s phone number is often used as the account number, and in similar fashion to a current account that is credited before using a debit card, the mobile account is topped up. To initiate transactions, the sender inputs the recipient’s details and the amount in a format of a text message and can transfer funds to other M-Pesa users and even non-registered users. The digital wallet was successfully introduced to other countries within the region including Tanzania, with similar environments to Kenya.

M-Pesa's mobile payments app

Remittances

The remittance industry is focusing on increasing convenience and speed for consumers globally, a result of technological advancements such as faster payment rails, smartphones and increased internet connectivity. According to the World Bank, total remittances sent in 2018 globally reached an all time high of $689 billion, of which the MEA markets received $108 billion. The MEA region is one of the fastest growing remittance receiving markets, averaging over nine percent growth during 2018.

The growth is being catalysed by the shift in migration patterns as more people move outside their home countries and contribute to the development of their home economies by sending money. While this behaviour is long established, customers now expect to be able to send that money digitally, like they do everything else. However, one of the challenges remains the high costs associated with remittances, particularly to the MEA region. For example, Sub-Saharan Africa reportedly has the highest costs, averaging at nine percent to send £200, compared to the global average of six percent.

Fintech startups including Denarii Cash (UAE), STC Pay (Saudi Arabia), Remit (Uganda) and Paga (Nigeria) are capitalising on market conditions such as increased smartphone penetration and digital adoption, and finding ways to use them to reduce costs. Taking inspiration from the likes of TransferWise in the West, mobile money operators are increasing the levels of competition by using fees and transparency as tangible differentiators to incumbents like Western Union and banks (which are the most expensive remittance providers). By building their business models on digital platforms, alternative providers have lower fixed costs, which they can pass onto customers. These providers also offer consumers quicker turnaround times by using technology such as APIs.

In this market, time, transaction cost and payment status are driving factors, and that means consumer behaviour is shifting from traditional methods of using kiosks or agents to a preference for digital alternatives.

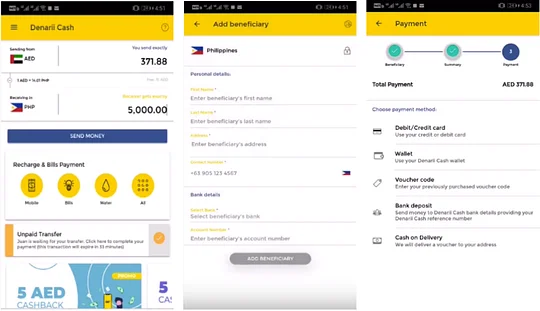

Denarii Cash

One of the new entrants competing with incumbents is UAE-based mobile app Denarii Cash. Launched in 2017, it offers simple, speedy money transfers with cheaper rates and transparent fees.

The app was developed to target Filipino expats in the UAE and Saudi Arabia after the Denarii Cash app founders realised a gap in the market as the highest inward remittances in the Philippines were originating from these countries. Since launch, the app can now be used to send money to other countries including India and Mexico.

The user downloads the app, and has the option to register via email, Facebook or mobile number. The account can be loaded using payment cards, ATMs, vouchers or in cash at kiosks. Once an account is credited, money is sent and the receiver is notified by text. The money is received instantly in some cases and can be collected from banks or participating agents.

It allows overseas workers to send money to their home countries using a freemium model of up to $300 a month and a flat rate of $2.50 for anything higher. Offering transparent fees, the model also employs a one-percent exchange rate, and a three-percent commission from the merchants that provide services on the platform. That means the app is attractive to senders as it offers better exchange rates while the recipient receives a larger amount than if the same amount was sent using incumbents, which absorb a portion of funds in fees.

Denarii Cash's mobile app (Source: Denarii Cash)