US Banking: Monzo rises to the challenge

It’s happening. After months of ‘will they, won’t they’, Monzo is heading Stateside.

I think we all saw this one coming. It was always a matter of who and when, not ‘if’, but congrats to Tom and the team at Monzo for getting there first. Will they be the challenger banking Beatles?

Plenty of the new kids on the block are lining up to take a crack at the US. But this isn’t exporting a musical phenomena; it’s banking, the thing we have in order to do something we want. The US also has plenty of banks, of the large incumbent varieties, the regional players and the shinier challenger shape.

Sure, we can laugh from afar at the lack of universal contactless payments, the continued use of cheques (sorry...'checks') and cash ruling everything around me...dollar, dollar bills, y’all. But these are ingrained behaviours that are going to be difficult to change.

Monzo is making all the right noises about launching small to understand customer needs and growing from there. They’re taking the community-based approach, including events in Los Angeles - where they are based - New York City, and San Francisco in the coming weeks to launch its card in the US and get direct feedback.

That’s smart as they are comfortable with that approach; they can act like a start-up and build, iterate and build again.

My question is...is that enough?

If you highlight, at launch, how different the market your entering is, will the same approach to growth also work? As Steve O’Hear noted on TechCrunch, Monzo has attracted a number of significant US investors including, most recently, Y Combinator. I expect they will lean on them to understand these nuances and challenges.

Monzo is making all the right noises about launching small to understand customer needs and growing from there

To state the obvious: the US is not like the UK. It doesn’t have a regulatory driver to encourage the take up of these services, it’s all market forces. It doesn’t have a fintech hub like London, a fertile ecosystem where so many of these new firms have grown.

The talent, the culture, the founders, the VCs, the law firms, all the things that make it work here are spread all over the continent. From Silicon Valley to New York, via Charlotte, North Carolina.

If we look at the successes to date - Monzo, Starling, Revolut - they’ve been built around an ‘outside’ proposition that looked, acted and worked differently. That could be advantageous verses the US incumbents but the US has plenty of its own challenger propositions that haven’t made a major dent.

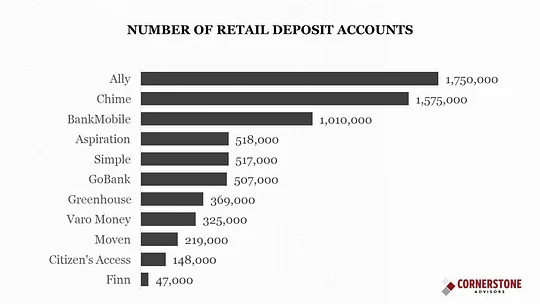

Look at this chart from Ron Shevlin at Cornerstone: these aren’t amazing numbers.

Source: Cornerstone Advisors

Perhaps being just slightly ‘better’ than Simple, or even Venmo, and having all of those capabilities in one app will be enough to get traction. As in the UK, I don’t expect them to be anyone’s primary account for a long time, but a secondary account for users in the large urban areas? Sure, I can see that.

Chime, an 11:FS favourite and winner of a recent Pulse Award is showing what's possible, with more than two million accounts opened and adding new customers faster than Citi or Wells Fargo.

So, assuming Monzo can get to a couple of million users, whether as primary, secondary or tertiary accounts, how do they grow beyond that?

It’s going to need a better digital experience, a rewards program, a savings rate that will challenge the likes of Marcus by Goldman Sachs, and offer the financial management tools many expect as a standard.

The other question has to surround how you market the proposition without that central community to grow from. This narrative of “yeah but we don’t really ‘do’ marketing” is all well and good when you’re building an audience in London. Stating you don’t want to rely on paid advertising in the UK is a fine notion but this isn’t the UK.

Now, I’m not suggesting Monzo or anyone else should sponsor a NASCAR team, do Superbowl halftime ads or put their logo on an NBA uniform. Equally, I’m not convinced the model they’ve used to such success here will necessarily work there to cut through the noise and the apathy.

Goldman Sachs spent a huge amount on marketing Marcus, even though it had brand affinity and the product hooked users by offering an above-average interest rate.

Monzo are doing great things but that momentum and success, and how it was built, is irrelevant to the US. I’d be happy to be proven wrong on this as the US market could do with a shake-up. I’m just not sure they’re going to take the US by storm in the same way, not for lack of trying but because the market isn’t there - yet.