Lending in Africa: The Good, the Bad and the Ugly

I’d like to start this by stating that Africa is not a monolith and for the purpose of this post, I’ll be zeroing in on the East and West African markets. This is taken from our Unfiltered newsletter. Subscribe now for a no BS, uncensored analysis of fintech news and hot topics delivered to your inbox each fortnight. |

Consumer lending and credit have existed in informal economies long before modern credit scoring and the traditional banking models we know now. Borrowing money with an interest attached has been well documented throughout history and exists today in even more complex and niche iterations than ever before. This is also true in African economies and communities.

The majority of African consumer spending exists in a “Pay-as-You-Go” model. Meaning, when you earn an income, you spend what you have to survive. This on-demand system can be seen in the way people pay for utilities, phone bills, and other day-to-day expenses. People spend what they have. But as time has gone on, more and more Africans have adopted the use of credit to supplement lifestyles and business.

The north star of financial inclusion has seen a number of fintech providers enter the space when the financial inclusion fuelled frenzy descended upon the lending market throughout the 2010s. After over a decade of experimentation, the dust has settled enough for us to take a closer look at the good, bad and ugly outcomes of digital first lending in the region.

Financial service providers who have managed to nail lending in Africa have tailored offerings to their markets that adopt a de-colonised approach...

The Good: |

Financial service providers who have managed to nail lending in Africa have tailored offerings to their markets that adopt a de-colonised approach, which disregards the sequence of product evolution we’ve seen in the global north. While the global north popularised the use of consumer debt via credit cards, African fintechs have taken a different approach: |

Carbon (Nigeria)

Tugende (Uganda)

|

The speed and ease of access to credit through mobile applications has caused many borrowers to become heavily indebted.

The Bad and the Ugly: |

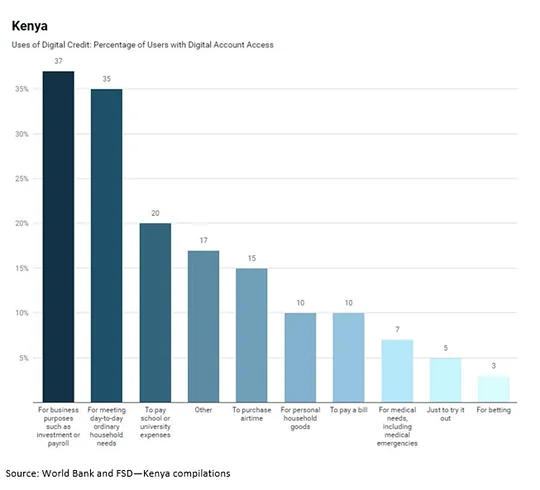

The World bank defines financial inclusion as access to useful and affordable financial products and services, delivered in a responsible and sustainable way - this rose from 26.7% in 2006 to 82.9% in 2019 in Kenya, driven largely by the growth of mobile money and fintech market entrants. A 2019 survey on digital credit found that 13.6% of Kenyans had borrowed loans from a digital lender, citing their convenience and ease of access. The speed and ease of access to credit through mobile applications has caused many borrowers to become heavily indebted. In Kenya, 20% of borrowers struggle to repay their loan. This is double the rate of loans from traditional banking. This is the bad and ugly side of truly digital lending and business models. |

Amidst the fintech frenzy, some players have emerged whose impact has resulted in a net negative for countless Africans. Here’s an example of one such fintech:

Tala (Kenya)

- Tala offers proprietary alternative credit scores and micro-loans to people in underserved markets such as Kenya, Tanzania, India, and the Philippines.

- The market has historically been poorly regulated with no caps on interest rates. Tala’s are typically 180% annualised.

- Tala targets the “bottom of the pyramid” of underserved populations that are less likely to be financially literate.

- Tala’s collections department has been known to contact borrowers’ family and friends when seeking repayment.

Traditional business models for credit and lending in Africa and other global south markets have been shaken up and reimagined, but the players who’ve done this in the most sustainable way have de-colonised their approach to a traditional business model by doing the following things:

- Embracing truly digital business models: Leveraging technology such as data and algorithms to assess risk and digital customer experiences

- Adopting alternative credit: tailoring scores to niche segments within their chosen market.

My unfiltered opinion

We can’t talk about Africa without talking about neocolonialism. Global north business models and practices have long been seen as a benchmark for progress in Africa and other markets in the global south. The future of finance in Africa relies on rejecting a trajectory that has been seen as “the norm” in the global north and instead building products and services from scratch that meet the customer where they are.

Africa has recently entered an era of consumer lending; facilitated and scaled by technology that has leapfrogged traditional banking and business models across Africa, resulting in mass adoption that hasn't followed the path of traditional lending in the west. It’s a start and we haven’t even seen 1% of the impact yet!