Open Banking in the UK: what's happened so far

Introduction

The first step towards banking automation came in 1967 following the installation of an ATM in the UK. Over 50 years later, Open Banking arrived, ushering in a new era of digital banking, which ironically is lessening the need for ATMs.

It is no secret that the financial industry was in dire need of a makeover, I mean except for a few bankers (if that), no-one really understood how most of banking worked even though it plays an integral role in our everyday lives. The 2008 global financial crisis was evidence of that and this disaster led to a review of regulations, from which Open Banking – the first enactment of PSD2 – was birthed.

Since January 2018, we have heard a lot about Open Banking, the regulation that has released the financial data of consumers from the banks’ ownership and into the hands of consumers. That means regulated banks in the UK are now required to let customers share their transaction data such as spending habits and regular payments with authorised third-party providers (TPPs) offering other services – as long as the customer has given permission. This is done in a secure manner through the use of Application Programming Interfaces (APIs), which provide TPPs with access to banking systems and customer databases. This allows end-users to manage bank accounts via third-party service interfaces that do not belong to the primary bank. There has already been a lot of discussion on what it is and how it will revolutionise the financial industry going forward, so I will skip all that and focus on the impact that it has had on the UK banking industry thus far.

Many of those in the media and the financial industry are still questioning whether there has been any change as a result of Open Banking’s implementation. The short answer is “Yes, a lot has changed.” It took us over a century to build the mess that was the banking industry, especially the lack of transparency for consumers, and somehow Open Banking is expected to result in a complete overhaul in one year (go figure). We can liken this to how contactless cards are now an essential component of payments, yet they were only initially introduced in 2007. The massive rates of adoption we’ve seen (and even then only in some countries) have only occurred in the past three years. Change takes time and the wheels are in motion.

Open Banking has brought a lot of significant propositions that were impossible two years ago to market. The use of open APIs to expose various data from a bank to TPPs has become one of Open Banking’s great achievements. To assist with delivering Open Banking, the organisation Open Banking Implementation Entity (OBIE) formed by the Competition and Markets Authority (CMA) have developed a suite of tools to enable firms to join the Open Banking ecosystem, share data securely and swiftly via the APIs and implement the standards consistently. More in-depth analysis on Open Banking APIs can be found here.

Ecosystem Players

Open Banking platforms

In response to the introduction of Open Banking standards, a lot of financial services providers launched their own Open Banking platforms. These platforms enable access to various banks in different countries through a secure, single API.

One of the largest such platforms is offered by payments firm Klarna, the most valuable fintech company in Europe as of August 2019. The firm offers a range of online services including direct payments, instalment plans and pay-later options, for both consumers and businesses. Klarna’s XS2A API enables access to more than 4,300 banks across 14 European markets and can be used by fintechs and other businesses, to develop, test and bring new services and products such as payment initiation and switching services to market.

Volt, a Dutch payments provider, is another platform which operates across 14 markets and enables TPPs access to over 4,000 banks. By connecting to this platform, these TPPs can perform a range of services such as the ability to initiate payments on behalf of consumers.

The significant advantage Open Banking platforms promise to the industry is the ability to empower consumers by increasing their ability to find new products and offering clarity over their finances and, in doing this, bringing the focus back to customer needs. Firms can meet this goal by connecting to the platforms in order to develop offerings like payment initiation, new credit products, advisory services and the ability to switch between mortgage providers.

What is also interesting is that in an effort to maintain their positions in this ever-changing market, card scheme providers are also looking at ways in which Open Banking can expand their offerings. Mastercard recently launched suites of Open Banking applications and has four separate offerings, which include verifying the real-time status of TPPs and an advice centre for banks building out Open Banking strategies. Educating consumers on the potential benefits of Open Banking will be critical to enabling adoption at scale and the platform aims to assist banks in this. As an organisation with a global reach, it will be helping banks explore and access solutions that are safe, reliable and trusted by customers. By entering the Open Banking ecosystem, it can also provide the nascent sector with expert advice – especially regarding data security, one of the key concerns when it comes to consumer adoption. Therefore, an organisation that already specialises in payments technology and securing consumer data will support adoption.

Such platforms are essential components of the Open Banking ecosystem, as they assist both financial institutions and TPPs navigate the opportunities and challenges presented by the API economy.

Third-party providers

PSD2 has identified two types of TPPs; Account Information Service Providers (AISPs) and Payment Initiation Service Providers (PISPs). An AISP is any business that uses a customer’s account data to provide services such as aggregating financial information in one place, tracking their spending or planning their finances. A PISP is any company that initiates digital payments on behalf of the user, directly from their bank account, offering an alternative to the use of a card.

All TPPs wishing to connect to bank APIs have to be authorised by the UK’s financial regulator, the FCA and can be found on this register. There were 137 regulated providers, made up of 85 third party providers and 52 account providers, and 32 regulated entities with at least one proposition live with customers by the end of June 2019, according to OBIE. This is in comparison to 57 regulated providers, 36 TPPs and 21 account providers a year earlier, evidencing the growth of the ecosystem and potential for its use.

So far, AISPs are the most common type of TPP, and a lot of the changes enabled by Open Banking that this report will explore are heavily linked to AISPs. Some of the services and tools that are associated with ASIPs include; price comparison, money management tools, quicker and more accurate access to financial products and speeding up manual processes such as applying for a mortgage, a loan and so on.

Services already being offered by banks

A single view of accounts

Account aggregation is the most common implementation of Open Banking so far, as account information APIs were the first type of API mandated on the CMA9 banks. It is a service which many customers including those unaware of this regulation are taking advantage of. Those customers that have adopted account aggregation found the benefits of keeping track of many different bank products in one place out-weighed the reluctance to share their data.

The initial focus was just on debit accounts; however, banks found customers needed to see different types of accounts in order to get the most use out of the products, and are starting to include credit and savings account aggregation. Lloyds has already introduced this feature to its app, and Monzo will be rolling out this functionality soon. It should be noted, however, that though open banking will be applied to this, this functionality is still largely achieved via screen scraping.

Aggregation also paved the way for new personal finance management (PFM) tools, something newer market entrants built in-house, from the beginning as part of their customer acquisition strategies. PFM tools and the best-in-class offerings in this space were already extensively covered in a previous report.

PFM

Traditional banks have done well at providing basic payments functionality and infrastructure but arguably have done less well at helping customers effectively manage their spending. PFM tools help with this by providing insights into spending habits and guidance around budgeting and savings they can garner from accessing transactions. HSBC was the first UK incumbent bank to offer PFM tools via it’s Connected Money app, which lets customers view their accounts at up to 21 different banks; however, this is done via screen scraping. Other providers in this space include Yolt, built and owned by Dutch bank ING, which is integrated with all CMA9 banks and many more. It also offers a marketplace of services, connected via APIs, and payment initiation services.

The Open Banking ecosystem

A change in business models

Challengers vs. Incumbents – who benefits most?

On the surface, Open Banking plays into the hands of challenger banks as connectivity and agility of this nature are very much their domain; they are selling themselves on their technology and the ability to provide integrated, on-demand and tailored services. At the same time, the regulation was widely hyped as bad news for incumbent banks as it risks turning them into commodity providers. That’s because most banking solutions are outdated, and interfaces are not intuitive. However, Open Banking APIs offer real opportunities to deliver innovation internally. It has provided mainstream banks with the opportunity to increase loyalty by offering their customers the best-of-breed products and services via already widely-used APIs.

That said, the enforcement of Open Banking threatened the very existence of the traditional banking business model and incumbents couldn’t help but resist. Deadlines were met with excuses, case in point, five of the UK CMA9 having to be issued with warnings after failing to implement Open Banking functionality meant to allow third parties consent within their mobile apps by March 2019.

A lot of the resistance has been blamed on the lack of clarity and the debates around how to comply. It could also be argued that incumbents were non-cooperative as they felt it was not in their best interests to actively engage in something that offers new challenger brands even more opportunity to disintermediate them.

One thing is becoming evident though, the incumbents have come to the realisation that their disdain for Open Banking is not going to stop it, and if anything it will only slow their progress in addition to costing them a lot of money in hefty fines for failing to comply, not to mention the potential loss of customers. This has resulted in a tangible shift on the part of banks, who are now viewing Open Banking as an opportunity to compete and innovate, rather than a compliance exercise. This is evidenced by the number of incumbents introducing account aggregation.

Open Banking: Innovation vs. Compliance

Partnerships and platforms

Open Banking has brought about new business models including deep partnerships and marketplace banking. It is safe to say, it was about time customers were offered such options in a space as important as personal finance and banking. This model offers convenience to customers as they have a digital shop window for the best products and services on offer in a single place, irrespective of who supplies them.

On the banks’ part, Open Banking has allowed them and their partners to build platforms that include integrations with other service providers, enabling them to build up their offerings faster and create a one-stop-shop without having to develop additional proprietary products. Challenger banks took to this idea with alacrity – Monzo developed a dynamic API system from the beginning, allowing different fintech front-end systems to communicate with its back-end core systems. Starling built a marketplace which features insurers, mortgage brokers and many other kinds of financial services providers.

The success in the retail sector with the likes of Amazon, and the convenience marketplaces have brought customers in banking has led to incumbents also starting to adopt this business model. This is because it allows them to find new revenue streams by enabling third parties to bring products to market faster. The marketplaces being built by some of these incumbents will be covered later on in the report.

New demographics

Open Banking is providing opportunities for banks to cater to underserved segments, and SMEs have particularly benefited. When it comes to businesses, they are typically heavily reliant on accountants for money management. But startups and incumbent banks alike are starting to offer services that reduce the need for expensive accountants, and they are going further than account aggregation to SMEs – Tink and Asto also offer PFM and analytics, for example.

When it comes to larger businesses, BBVA One View, is a real-time platform service that allows businesses to control all their domestic accounts, credit accounts and cards from a single dashboard. All this and more has already been extensively covered in a report of such SME offerings and can be found here.

Services being offered by TPPs and startups

Debt management

Debt management is one area of financial management that consumers continue to struggle with, as banking providers do not typically offer easily accessible services. This is starting to change thanks to Open Banking.

Startups such as Tully are using the regulation and associated technology to improve debt management. Tully aims to bolster financial education and offer customers tailored financial plans to tackle debt. The organisation was granted an AISP license by FCA which allows it to pull in consumers' financial data, enabling it to build an accurate picture of the customer’s finances, and in turn, apply the findings to the tailoring of plans. Big banks are seeing the value of such services, as evidenced by incumbent Nationwide partnering with Tully as part of its "Open Banking for Good" initiative.

Another platform utilising AISPs to assist with debt management is OpenWrks, a financial advisory platform that can access a customer’s bank account information to assess their financial situation in order to offer tailored advice.

Such services go beyond just helping customers in debt better manage money, extending to provide specific tools to help people prepare for mortgages for example. These tools can have a big impact on customers’ lives – by taking control of their finances, consumers stand to save up to £2.7bn a year, an average of £287 per person, which equates to an average of 2.5% of income, according to a report by OBIE.

Offering intelligent insights, budgeting and control tools assist customers in making decisions regarding the debt that will promote financial health and this has all been made possible by the introduction of Open Banking.

Lending

The use of Artificial Intelligence (AI) in finance is growing across a number of areas including lending, but it requires large volumes of data in order to enhance the associated processes. The introduction of Open Banking allows lenders that are also AISPs access to a much larger pool of data which was historically impossible, and which when combined with AI, allows lending recommendations for a wider range of customers, changing their experience in this sector.

Lending has already been significantly positively impacted by Open Banking related initiatives. So far, Open Banking has enabled: convenience and speed, transparency, better tools for lenders, marketplace integration and tailored services to this sector.

P2P lending

P2P lending platforms such as Zopa, Growth Street and RateSetter, geared towards both consumers and businesses, have enthusiastically embraced Open Banking. These platforms provide borrowers with a new way to access finance and facilitated loans worth nearly £3 billion during 2018.

P2P lending platforms have embraced Open Banking

Each platform applies Open Banking to various aspects of their businesses, with the aim of making products and services better tailored to their core customer bases. Growth Street uses Open Banking to assess the financial history of potential borrowers and to help monitor their cash flow and financial strength, for example. The recent partnership between Starling and Growth Street allows the bank’s customers, with a GrowthLine product, to view real-time information on their facility within the Starling app.

Another use of Open Banking by these platforms is partnerships with credit agencies to streamline loan application processes – Zopa launched its own verification tool in partnership with TrueLayer, for example. That negates the need for borrowers to upload documents manually. The lender reports that over half of its customers select this Open Banking-powered verification option, a sign that consumers are responding positively to the tools and services enabled by this new regulation.

In a similar manner, by partnering with AccountScore and Equifax, the Freedom Finance platform is able to notify personal finance providers of real-time changes in a customer’s circumstances that could alter eligibility.

SME Lending

Open Banking benefits have not only been limited to consumer lending but brought much-needed relief to the SME sector.

The UK SME segment is comprised of 5.7m businesses and, despite being deemed the backbone of the economy, access to working capital remains an issue. It stems from the period after the financial crisis, when incumbent banks cut down on the amount they were lending to SMEs owing to the cost of underwriting. Open Banking has enabled a variety of solutions to address a number of SMEs’ capital pain points.

To start with, platforms such as Funding Options and Freedom Finance use Open Banking data to detect how an SME is performing and the likelihood of a default based on factors such as current account performance, cash flows and other behaviours. Following the assessment, the SME is offered a range of lenders best suited to meet their needs.

To further enhance its business offerings, challenger bank Starling recently expanded its marketplace for SMEs i.e. its partnership with SumUp provides small merchants access to faster settlements. By capitalising on Open Banking, Starling was the only banking provider (by August 2019) of real-time access to Faster Payments through APIs in the transaction banking world.

The success of new market entrants has encouraged incumbents to adopt similar models. Nationwide, Santander and TSB are some of the incumbents working on increasing solutions to address SME needs regarding cash flow and have a specific interest in marketplace lending.

Open Banking allows lenders to take into account business performance and not just credit score, making it faster and less-risky to lend to SMEs. This is important as SMEs’ cash flow is typically variable, which affects the firm’s overall credit score and in turn, limits access to working capital. US-based fintech Kabbage, which operates a white-labelled model in Europe has a partnership with Santander offering UK SMEs loans of up to £100K within minutes. Kabbage’s platform was built in-house and the company incorporates real-time risk modelling, which is used to cross-reference customer data against multiple sources such as social media.

Another advantage of a platform like Kabbage is that it allows customers to draw down credit as often as once a day, until the approved limit is reached, meaning the business owner can access working capital at the point at which they need it.

By partnering and integrating with alternative lending facilities, banks can increase customers’ options if they are unable to provide the appropriate lending themselves. Barclays and Santander took stakes in fintech challenger MarketInvoice, for example, and launched online invoice finance options for their business customers in partnership with the startup. Similarly, TSB chose to partner with Funding Options to offer a business marketplace tool on its website for business customers to seek out alternative routes to finance. The end goal for these banks and the likes of Starling is to continue building comprehensive marketplaces that incorporate lending in a bid to create a hub for small businesses. This both encourages customer loyalty and brings the banks new sources of revenue as they typically take a share in the lenders’ fees.

Alternative lenders

The end-to-end process for SME loan applications was historically very lengthy. That’s problematic because the ease and speed at which an SME can receive working capital is critical to the survival of the business. However, alternative finance providers such as Iwoca and Kabbage are using Open Banking to speed up the borrowing process and make life easier for SMEs.

By incorporating transaction data into applications and risk models via Open Banking (thanks to its AISP license), SME lender Iwoca allows its users to complete a loan application for up to £150K in as little as 15 minutes through an automated lending platform. It was the first lender of its kind to integrate Open Banking APIs and take advantage of partnerships with CMA9 banks including Barclays, Lloyds and HSBC. In addition to incumbents, Iwoca also partnered with neobank Tide to offer customers loans immediately after onboarding, with the approval process taking as little as two minutes.

One of the biggest disadvantages associated with incumbent banks’ lending processes is that they take a one-size-fits-all approach with smaller businesses, which results in many SMEs being unable to access working capital. This is where digital lenders can solve another pain point, by leveraging Open Banking to offer tailored solutions to each business. And the model is working – Iwoca reportedly accounts for a 12% market share of new SME loans.

Iwoca’s process provides a great example of how Open Banking can improve user experience. It goes as follows; a business owner applies for a £10K loan and if they are not eligible, it can be determined in seconds using data pulled using Open Banking APIs. The eligibility checks will then calculate an amount that the business can be offered. That means instead of letting them proceed with the application and declining them the loan, Iwoca will offer an alternate amount, that they are eligible for, let’s say £5K. This approach gives the owner an opportunity to change the amount before submission, therefore raising the chances of approval.

The approaches being used by these alternative lenders, which are based on banking data are particularly useful for increasing lending volume of near-prime and thin-filed borrowers. They are transforming the way lenders have historically evaluated individuals' creditworthiness, which had previously changed very little in the past three decades.

Lenders currently using Open Banking are already seeing benefits in the speed and number of applications they can process and accept while getting a head start on understanding its implications for credit risk modelling. The future is here, but it's up to forward-thinking businesses to capitalise on it.

Overall, the landscape of SME banking has dramatically changed since the introduction of Open Banking, including account opening and KYB processes. I will not go into more details regarding onboarding or SME banking as these were intensively covered in previous reports.

Mortgages

Mortgages remain one of the most important financial products for consumers and the process is historically known to be laborious and stressful, both for first-time buyers and when remortgaging.

The complexities associated with getting a mortgage are mainly attributed to the many different players involved in the process i.e. the lender, broker and lawyer. With all these services coming from different providers, it can be very difficult to achieve a seamless experience and requires the customer to be simultaneously dealing with multiple service lines. So it’s no wonder that the mortgage system is broken and a painful experience for customers. The question is why, especially in an era of financial disruption, has little been done to improve an obviously broken system? The simple answer is there has not been a major driver for lenders to do so, as they have faced little competition in this area. That’s in contrast to transactional banking where there has been a great deal of disruption caused by new market entrants, leading to lenders feeling an urgent need to make improvements to their own products and services. That said, it is surprising that such a high level of borrowing commitment has not been given more attention.

Broken mortgage processes are an issue Open Banking has started to address and various new players have entered the market. The benefits Open Banking offers to the mortgage industry include tailored experiences and the transformation of numerous tasks all throughout the process. That’s because easier access to increased volumes of data can go a long way towards enabling firms to re-design lengthy mortgage application forms. It can help with pre-populating fields, while access to real-time financial data allows lenders to make behavioural decisions and build more predictive, consumer-friendly and personal services.

Brokers

Incumbent brokers are largely still struggling to adapt from a mainly manual model to more efficient technology-based solutions. One of the key hassles, not only for customers but also brokers and lenders, is the paper-based processes that have remained a part of the industry. However, this is one of the easier areas of mortgages to disrupt as these processes can be easily automated and when combined with Open Banking, have the potential to transform the industry.

That’s sparked the rise in online mortgage brokers like Habito, Mojo and mortgagegym which have stepped into the gap in the market. They aim to make the mortgage journey for customers faster, more transparent and more efficient.

In an effort to improve the mortgage journey for customers, Mojo is developing a same-day product offer utilising Open Banking by analysing everyday spending through account integrations. One of its recent integrations is with challenger bank Monzo, which it hopes will assist with offering remortgaging advice. Mojo has been vocal about centring its propositions around Open Banking and is exploring new ways to extend its services using this regulation.

When it comes to eligibility checks, most lenders are unable to check an applicant before the money is spent on credit checks. This is also the area where the likes of mortgagegym have been making improvements to smoothen the mortgage application process. It became the first firm to combine Open Banking, credit file searches and bank accounts to check for consumers’ eligibility by looking at spending patterns and matching it to what is stored on their credit file. Mortgagegym is integrated with 12 lenders and credit reference agency Experian.

By using Open Banking, mortgagegym enables homebuyers to complete their entire application online in as little as 15 minutes. By analysing an applicant’s 12 month period spending patterns, the broker can present potential buyers with mortgages they can definitely afford. Meanwhile, traditional lenders are only using a three-month period, which lessens the options available to prospective buyers.

Also, in this space is London-based mortgage adviser LDNfinance, which started using Open Banking platform to speed-up loan applications. It partnered with LendingMetrics and employs its OpenBankVision (#OBFREE) platform which gives it real-time access to applicants’ bank statements and transaction details. This process eliminates the need for physical copies of documents and ensures checks, such as those for affordability, are accurate. Through the use of categorisation tools, data can be filtered to automatically identify salary payments and ongoing commitments, reducing the time to assess creditworthiness to seconds.

Doing away with paper – tradition vs. digital?

The entrance and success of these digital brokers is forcing traditional brokers to adapt or risk losing market share. With a dominant market share, brokers are aware that in order to maintain it, they need to ensure they are investing in the right technology so as to defend against disruption. This has led brokers such as London & Country to launch an online application process in order to keep up with newer entrants. The traditional players, however, should note that simply making the process digital is not enough to retain customers.

How the mortgage process is being simplified

Lenders

Incumbent lenders are also starting to use Open Banking – Bluestone mortgages became the first mortgage lender to use Open Banking as part of its core underwriting process in early 2019. By partnering with Experian, customers will be given the option to provide their bank transaction data to Bluestone within minutes and therefore reducing the mortgage processing time.

Following its success in the brokerage space, Habito decided to expand its services to lending after receiving regulatory approval to become a mortgage lender in 2018. Habito developed its own proprietary lending platform, which it hopes will cut the time from mortgage application to offer in half, by addressing some of the broken aspects of the process. Its first step into mortgage lending will be providing buy-to-let mortgages in partnership with an unnamed financial institution. Habito should not only guarantee a quicker application process but also does away with the need for physical copies of documents to be passed back and forth, as it serves as both the broker and the lender.

An interview with Habito’s CEO Dan Hegarty provides a more in-depth insight into their lending vision, including the platform’s feature Instant Decision, which was devised to replace the mortgage “Decision in Principle” and is deemed to be more reliable by the broker.

As in other disrupted sectors, incumbent banks are being forced to adapt their business models and start offering value-added services in the mortgage arena. M&S Bank was one of the first UK incumbents to introduce Open Banking to its mortgage application process. This implementation does away with the need for physical bank statements to support the mortgage applications and this is achieved via a partnership with Equifax and AccountScore. By doing this, the incumbent is extending its use of Open Banking, which it already applies to its loans and credit card applications.

Incumbents have to also be mindful that it’s not only newer market entrants that will take advantage of disrupting the industry using Open Banking, but other players might consider entering the mortgage lending space. This has been the case in the Netherlands, following from the financial crisis, when non-bank lenders such as insurance companies entered the market as direct lenders and now account for over a third of all mortgages.

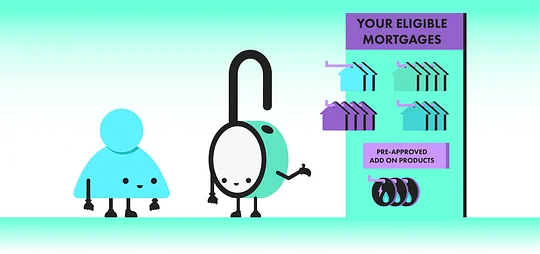

Open Banking has not even scratched the surface when it comes to mortgages. Currently, an end-to-end mortgage solution does not exist in the UK, but when one comes to market, it will not only disrupt current business models but is likely to quickly secure its position as a market leader. This could be achieved via Open Banking integrations, and will likely be similar to a system already successful in Norway.

Also, by taking inspiration from the fintech scene, a digital mortgage marketplace might be the answer to mend the broken system. Customers could be provided with the most suitable mortgages at a competitive price, while at the same time ensuring eligibility on application. Market places also could add value to customers by having intermediaries on their platforms which can offer other, complementary products such as home insurance and utility deals.

What a mortgage marketplace might look like

A2A Payments, PISPs Breaking the value chain

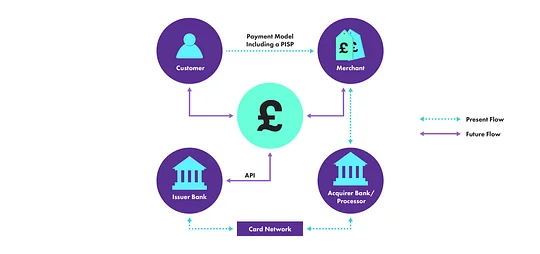

The payments sector was one of the first to be disrupted and that has continued at pace as fintech has taken hold. Now, thanks to Open Banking, that disruption is likely to pick up the pace again. Open Banking regulation has brought change to the way payments can be made. End-to-end services across the payments value chain have historically been solely provided by banks; however, paytechs and challenger banks are generating a refreshed interest in the payments space. Though the uptake of Open Banking in the payments space is still in its early stages, the value chain is dramatically being reshaped especially in the card payments sector.

One of the ways in which change is being brought in via PISPs, which initiate payments from a user’s bank account, with the consumer’s consent and authentication, to a merchant’s account. This removes the need for a traditional card acquirer and account balances are updated in real-time. The main advantage for consumers is the speed it brings to payments and the ability to more accurately know their financial position at a given moment in time, while for merchants, it's cheaper because it removes the merchant service charge (MSC) fees. MSC is a fee paid by the merchant to the bank (acquirer) processing the card transaction. More info on A2A payments and how they work can be found here.

Disruption of the payments value chain

Other benefits to consumers of using licensed PISPs, such as an app that assists with money management, can include making it less likely that they will become overdrawn. This can be done via automated money movement using tools that automatically transfer a customer’s money between accounts on their behalf to avoid overdraft fees. In a retail setting, connecting a retailer you regularly shop with to your bank account can result in faster payments through instant checkouts. Instead of interrupting the customer journey at the end of a purchase process, the payment would become an integrated part of the customer experience.

The use of PISP provided services has not yet quite taken off in the same manner as AISP enabled services; however, there are a few out there. Bud was one of the first to obtain a PISP license in February 2018 but the first end-to-end PISP transaction was not completed until June 2018, when Token used Open Banking APIs connected to Santander’s API payment initiation endpoints.

Other examples of A2A payments enabled by Open Banking that have been available for a while including the Swedish online payments firm Trustly and the German banking service Sofort. Payment company Adyen also extended its services to payment initiation in early 2019, by plugging into the CMA9 banks and allowing customers to select A2A payments. All these providers have long since established themselves as universal payment providers, and many online shops are increasingly using these new solutions to offer their customers additional payment systems.

When it comes to A2A payments, a move away from online card payments means a loss of revenue from fees for incumbent banks, both on the card-issuing as well as the card-acquiring side. However, this does not mean incumbents are ignoring the potential benefits. In June 2018, Citi became the first corporate bank in the UK to enrol in the Open Banking directory as a PISP, and Metro Bank launched its own API developer portal, the month after.

Meanwhile, in May 2019 NatWest became the first UK bank to use Open Banking to provide customers with A2A purchases. At the point of sale, the customer is redirected to the bank’s login page, where they can initiate the payment. This method also enables the customer to check they have sufficient funds before authorising payment. One of the biggest advantages of this technology is it allows bank-to-bank transfers using Faster Payments, therefore delivering immediate settlement for merchants.

We are starting to see progress in regards to A2A payments, which will only be strengthened by the SCA requirements deadline set for March 2021, an extension from the initial one of September 2019. This PSD2 originated initiative is increasing customer security by requiring online payments to be authenticated using 2FA. A more detailed explanation is provided on this blog. The deadline was initially outlined in 2015 and it has been met with resistance, with most incumbents citing the need for more time. As such, the EBA announced in June 2019 that some providers will have the deadline extended to them, and only in exceptional circumstances.

A2A payments may still be a long way from being the norm but we eventually started using debit cards more than cash so there is still time for A2A payments to follow the same pattern.

What’s next?

Despite talks of little having changed since the 2018 introduction of Open Banking, consumers and businesses have been benefiting in various aspects due to the enforcement of this regulation. Furthermore, the UK was the first country to develop Open Banking standards and remains the leader in this field. This has inspired other countries including Australia, Canada and Singapore to develop their own models basing it on UK experiences. Embracing Open Banking and APIs means that banks around the world can innovate quickly, keep pace with customer demands, and advance their customer experience in an efficient way.

That said, in order for wider adoption to occur of Open Banking enabled services, a change in culture and consumer attitudes needs to take place and the Open Banking ecosystem as a whole needs to show proof of success, establish trust and offer reassurance around the security of data. Consumers can gain up to £12bn a year from Open Banking enabled services, while the potential value for SMEs is £6bn, and the benefits are particularly extended to those who are overstretched in areas such as budgeting and working capital, according to research by OBIE.

To make the most of Open Banking, banks will have to actively engage in Open Banking innovation and forge fintech partnerships with companies using their data sets. That will enable them to enhance existing products and leverage innovative fintech products being created with their data which will, in turn, hugely benefit their customers. In addition, educating consumers on Open Banking, particularly its security, has to become a priority as they are a key factor to its success.