Why being loveable is better than being viable

TL;DR – Creating something new is hard, because the idea and design is the easy part. Anyone can have an idea. Getting it in the hands of the customer is the hard part. This is why a Minimum “Loveable” (not “Viable”) Product is your new best friend.

So, you want to do something really new?

At 11:FS, we tend to get called when large organisations want to do something shiny and new, something that moves the needle for growth and has a fresh perspective.

Why is this? When every bank, insurer or FI has a lab, ventures team, or some unit in charge of doing cool shit?

Bank labs are often staffed with tenured, talented and enthusiastic bank staff and external hires from tech companies, telcos and elsewhere. On the face of it, they’re set up to create the next generation of digital products and services.

Except they don’t.

Not because they lack talent, but because they lack a clear path to execute and the autonomy to do so. Don’t get me wrong, I think given the challenges banks have they do some impressive things.

BBVA has an excellent marketplace, the Dutch banks have done interesting spinouts (e.g. ING and Yolt, ABN and New10) but this job is 1% finished. There’s so much left to do. So much effort wasted.

Mind the culture gap

To the frustration of most of the talent in these teams, whilst the tools, interior design and uniform may have changed, the funding and mandate hasn’t.

It’s hard to allow teams to build like a start-up when something needs to be in scope for the program and its roadmap. Start-ups don’t need to write a 5 year business case and get 14 committees to approve. They need to build something that customers want, so they can secure more investment - and fast.

There is no talent you can bring into an organisation that can out-deliver a process which casts the product features in stone before a customer sees it. Everything in large organisations is designed to remove autonomy and spread accountability. It creates adversarial relationships between those charged with developing the new, and those who have to approve it.

The result is innovation theatre.

Thousands of busy internal meetings, countless powerpoint and spreadsheet outputs, and the same delivery engine, people and processes that were there last year. Delivering an upgraded version of what was there last year.

The “digital transformation” approach

The way most big organisations do “new”, is with “digital transformation”:

A research team/vendor speaks to some customers at a point in time and hand a report back to their client/other teams

The strategy team/vendor go and look at “best in class” and come back with a list of things other people do well

The design team/vendor start designing screens based on the strategy team’s feature list

The delivery team/vendor starts spooling up a team to deliver the capabilities

The software/integration vendors begin to analyse how the “new” thing would integrate with existing systems

They start aligning and “interlocking” plans and budgets and committees

There isn’t one team, or even company, that is individually empowered to deliver for a customer. The research team people who met the customer are so far away from delivering the actual product that important context and nuance goes missing.

The strategy team identify a market and an opportunity but often miss why customers love something.

The design team haven’t internalised the research or strategy because they never met the customers and may not have been involved in forming the strategy.

The delivery team gets thrown the requirements, which they in turn throw at vendors so they can interlock plans.

What does “digital transformation” deliver?

“Digital transformation” tends to upgrade existing capability rather than build from scratch. Because:

- Feature parity is not product parity

Digital transformation delivers the features fintechs and challengers make famous. Copying the feature without understanding the process that led to the feature development is a follower strategy. This strategy won’t drive the growth that start-ups enjoy because it exists in isolation to the rest of the offering.

- Fighting to get on the roadmap

Digital processes in banks and FIs have a limited capacity and must integrate with a myriad of legacy systems and vendors. They have demand from across a number of product lines and become a key bottleneck. This means propositions are always fighting for airtime and to get into already busy digital real estate.

Trying to do new, with the exact same approvals route to market as everything else won't create a step change: it will create a big disadvantage.

The big disadvantage of “digital transformation”

Banks become followers, not leaders.

Their products are unable to gain the growth that start-ups who focus on customers achieve, or that high growth tech companies achieve. This is a culture challenge and bias that needs to be overcome.

Great ideas never make it to market.

There is no clear way to capitalise on the learnings because the focus is on product viability, not loveability (more on that later).

Business opportunities are lost to new entrants and big tech. By the time a product feature has made it to the market, the market has moved on from where it was when the idea was incepted.

The start-up approach

Putting it simply, start-ups don’t think about integration to existing systems, customer call centre scripts or a target operating model. All the things big organisations spend a long time arguing about.

Our CEO David put it simply once when asked: “what’s the secret?”

Smart people making shit up

But to get the mandate for smart people to make shit up, you need to get a different mandate.

Rather than trying to do “new” in a new way, and having every project across the group try to be agile and “start-up”, pick one thing and give it space, autonomy and mandate.

In practical terms, we’ve seen this work with:

A real mandate - if you’re doing something new, and you’re changing how you do change, you can expect the organisation to want to kill it (e.g. Marcus by Goldman)

A mix of people who’ve done it before in start-ups and people from the bank with the right skills (not re-assigning thousands of people in one go) (e.g. Bankmobile originally with Customers Bank)

To deliver as quickly as possible a Minimum Loveable Product (e.g. Mettle by Natwest)

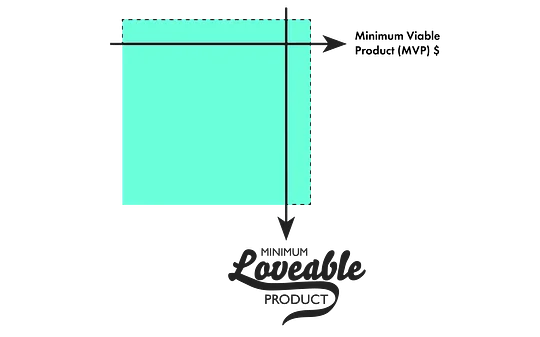

Introducing the Minimum Loveable Product Matrix (™)*

*100% not a trademark, but whenever I say something that sounds corporate bullshit-y, I kinda have to put that there.

(Those dotted lines are the slices of what you can do. Delivering an MLP requires fewer, but better, features.)

If the X axis is feature completeness and the Y axis is the depth of a customer job to be done that is solved for, a Minimum Viable Product (MVP) must by definition be viable. It is designed to drive revenue from customers and must be somewhat feature complete.

On the contrary, a Minimum Loveable Product (MLP) may not be viable at all. It is designed to drive user growth and iterate rapidly. Often it is not feature complete.

The fundamental difference is between scaling a product that had its features agreed in last year’s strategy planning and shipping something much smaller, much easier to mould where the features can be wrong, changed and emerge over time.

MLPs may launch with a product that could not be used at scale, but find it easier to fit within risk appetite, learn and adjust. It then bakes those learnings into future iterations.

MLPs may be manual (eek!), and it may use a fintech behind the scenes, not internal platforms (double eek!). But what matters is how quickly the product changes shape to find that thing a customer really loves.

Then - and only then - do you begin to scale.

Start-ups move faster than big companies because they embrace uncertainty and changeability in their “roadmaps” in how they deliver.

If you’re looking for secret sauce, there it is.

But how do you make that work with your roadmap?

(Hint: that’s the wrong question)

Red pill or blue pill?

Everyone loves a matrix, and the risk is you see Minimum Loveable Product as marketing bullshit. (I mean, we do have stickers and t-shirts with it on - bag one for yourself here.)

I guess my point here is that there’s a technical difference between the two.

The start-up approach is fundamentally different to digital transformation.

The Minimum Loveable Product is fundamentally different to the viable product.

And if it all seems like a bunch of buzzwords, let’s have a chat. Because I fear that, much like the matrix itself, nobody can be told what it is: you have to see it for yourself.

Want to chat to us about creating a minimum loveable product? We’re all ears - get in touch at hello@11fs.com, or check out our awesome guide to Minimum Lovable Brand.