Don't design financial products: design financial behaviour

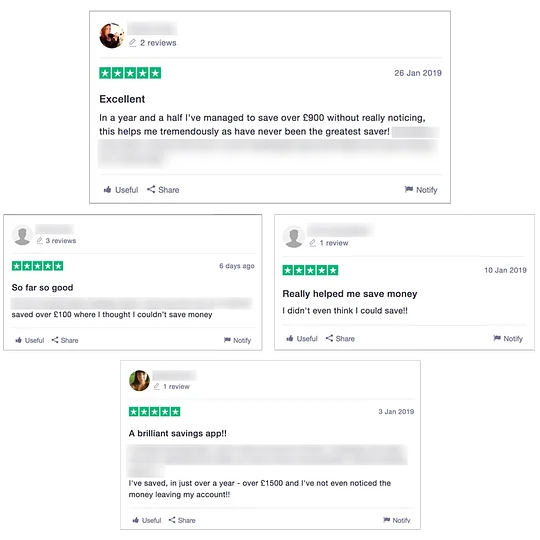

If you look at the Trustpilot reviews for Plum (the UK savings app), one thing stands out. People don’t talk that much about the product; instead, they proudly declare how much they’ve saved.

These users don’t really care about this app. They care about what they can do when they use this app. It’s not about features or UX or anything to do with the product at all: it’s about behaviour.

They’ve gone from being unable to save and feeling all the frustration of their goals always being out of reach, to the kind of people who can steadily work towards achieving the things that matter to them.

There’s loyalty – and then there’s being the catalyst that changes people’s behaviour so profoundly that it changes their lives, and changes how they think about themselves.

Who your customers really are

Behaviour change isn’t a new goal: healthcare providers and advertisers have been trying to shift behaviour for as long as these industries have existed in their modern form.

Then Behavioural Economics added some much-needed rigour to validating and quantifying the effects of behavioural ‘nudges’, and its pioneers were rewarded with a Nobel prize. Along the way, they demolished the previously-commonplace assumption in economics that people were fundamentally rational beings, AKA “homo economicus”.

Yet most of the financial services industry still treats its customers like they're perfectly rational. If they get the right financial education, the right product information, then they’ll make the best choice for their situation (and that choice is obviously our products).

But we all know that people are fuzzy-minded, biased and deeply irrational. They fall victim to the sunk cost fallacy when they throw good money after bad. They’re always more optimistic than experience tells them they should be, especially when they’re making plans for the future. They’re paralysed when confronted with too many options, and logical decision making goes out the window.

Bringing behavioural psychology into FS product design

When you design products that work with users' irrationality rather than against it, you design better, more engaging products. That’s the insight underlying the sky-high engagement metrics of the top social networks and the addictive qualities of slot machines.

And people are more irrational than usual when they’re dealing with money or thinking about the future. Psychologists and lay people have been discovering new ways in which our brains misbehave around numbers and money since some bright spark invented the £0.99 price point.

This is just one of the reasons why it’s so hard for people to do the right thing with their money. For instance, people know they should put money away for retirement, but their brains work against this good intention.

In a series of studies, people who are offered $50 today, or $100 in one year’s time almost always go for the $50 – because our brains have simply evolved to prefer immediate rewards over greater, delayed rewards. Exactly the same thing happens when people weigh up increasing pension contributions or having more disposable income today.

It means there’s a huge opportunity for financial services companies to use these behavioural insights to improve their products and – more impressive – make their customers’ financial behaviours more healthy. When you design your products with your customers’ 'cognitive biases’ (the quirks in how their brains work) in mind, you can actually make it easier for them to do the right thing than the wrong thing.

The Save More Tomorrow programme, co-created by Nobel-prize-winning behavioural economist Richard Thaler is a great example. Knowing people’s tendency to discount future increases in income, the programme asks employees to sign up to a company pension scheme that will increase their contributions every time the employee gets a pay rise. The employee still sees some extra money from the pay rise, so they’re still happy, and they’re contributing more to their pension without feeling like they’re missing out.

Integrating these behavioural economics and psychology insights into the design of digital services is known as behavioural design. It can be a daunting task, but with the right help it’ll feel simple.

Come talk to us hello@11fs.com, as proud behavioural designers, we’d be happy to show you how to deliver a product customers will love.