The State Of Retail Payments In The Americas

Newer firms are reinventing existing payment systems in the Americas

In this part of the changing global payments landscape series, I will be discussing how providers in the North and South Americas are using technology and changing regulations to reinvent some existing payment options to meet changing consumer behaviour.

The Americas are fragmented when it comes to payments, with the northern part having a more stable infrastructure, while most of the population in the southern parts has historically lacked access to formal financial services.

Though there are differences in infrastructure, there are some similarities in terms of payment trends, for instance the heavy use of credit cards across the entire region. Additionally, in line with a high penetration of smartphones across the region and the resulting changes in consumer behaviour and expectations, a lot of innovation post-financial crisis has been centred around mobiles. The general opinion is that more innovation has occurred in the north, but that may not necessarily be true.

Fragmentation within the region also applies to regulation, with various countries focusing on different regulatory initiatives. For instance, the southern countries are implementing new regulations that allow new companies to enter into the payments industry, as is the case in Brazil under its Payment Institution regulations, and in Mexico through the Fintech Law introduced in 2018. Meanwhile, there are currently more regulatory barriers for newer market entrants in the northern part as discussed by David Scola, who also cited some of the regulatory initiatives currently in play in the US.

This section will discuss how types of payments such as P2P and point-of-sale financing have been reimagined and are gaining traction in North America, while South America is finding alternative digital ways with which the masses can use to replace cash.

Peer-to-Peer (P2P) payments

In the late 1990s, PayPal brought the concept of electronic peer-to-peer (P2P) payments to the mass market in the US following the launch of its money transfer service, which aimed to boost e-commerce business. However, it has only been recently that this type of payment has reached widespread adoption via mobile applications such as Venmo, Cash App, WhatsApp Pay and Facebook Pay.

So why is it picking up pace now?

In short, smartphone technology simplified the process. Before smartphone apps, tasks such as paying back friends, splitting dinner bills or sending money were awkward and friction-filled as they required the use of cash or complicated, desktop based bank transfers. Now, the transaction can be initiated and authenticated all within an app, taking a matter of seconds. As the adoption of P2P apps increases, the range of purchases to which P2P payments are applied has grown to include bigger-ticket items.

P2P apps are common way to transfer money between friends

The P2P payment market in the US in particular is booming, with over 80 million estimated users and $220 billion processed through this method in 2019. The success of standalone apps has resulted in incumbents also launching their own apps, for example, Zelle which is owned by seven major banks. P2P payments will continue to be bolstered by the sharing and gig economy, which often involves short term P2P transactions to share use of assets such as cars and facilitate services such as renting extra rooms.

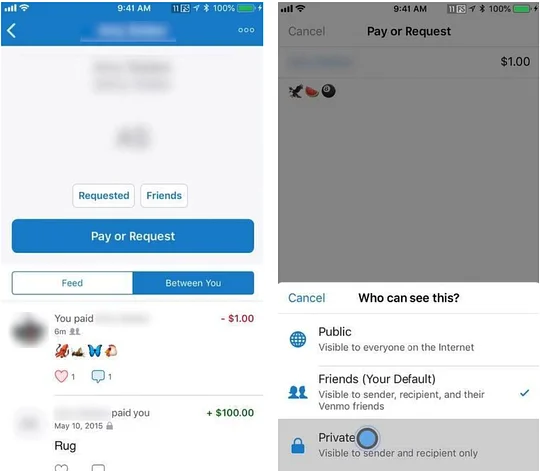

Venmo digital wallet

With more P2P options flooding the market, a combination of factors such as flexible pricing strategies and superior user experience are key to not only gaining new customers but maintaining the existing base, something Venmo seems to be doing very well. The company, now owned by PayPal, has a registered user base of around 50 million, and processed over $27 billion in payments during 2019.

It’s particularly popular with younger users, which is not surprising as it does not charge its users to send or receive money and offers a wide and increasing range of features and functionalities. Sixty-six percent of young Americans that used mobiles also reportedly used this app and it has moved from simply being an app to send money quickly, to being used for other transactions types such as roommates transferring shares of utility bills to each other. That has resulted in an increase in transaction size from an average of $2 in 2016 to $60 in 2018.

Venmo's mobile app

Point-of-sale financing

One payment method seeing a resurgence within the American region is point-of-sale financing (POS financing) – an industry now estimated at $391 billion a year. This form of payment, which often provides consumers an interest-free option to spread payments, is by no means new; however, newer market entrants fueled by new technology and similarly powered offerings by popular e-commerce sites such as Asos, along with a change in consumer attitudes, are contributing to increased usage.

Technology is arguably the key driver in the increased adoption of POS financing options. Algorithms and high-speed internet connections are enabling providers to check records and determine a consumer’s relative risk almost instantly. API connectivity is also playing a key role. For instance, some scheme options such as Klarna and Affirm have a mobile app on which consumers can browse all stores the scheme is affiliated with and shop via the same app. Furthermore, details such as addresses are only required when the user signs up for the service. After that, they only need to approve the purchase and can avoid the tedious task of entering card details, once again adding to the flexibility and convenience valued by consumers.

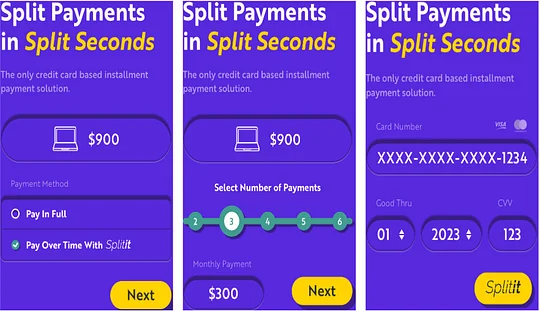

Splitit

Another scheme gaining popularity is Splitit, which can be used for both B2C and B2B purchases and allows customers to spread their repayments without requiring them to open a new line of credit. Unlike other schemes, with Spilitit, the user pays with their debit or credit card and no application fees for B2C purchases.

How does this work?

At the POS, the user selects Splitit as the payment option and is then redirected to its portal where they enter their Visa or Mastercard payment card details — which is convenient as the customer is not required to set up an account or download an app. They can then choose how many instalments they want to use to repay the cost of the purchase and these are then taken from their card once a month – over a certain interest-free period, up to three months for a debit card and 36 months for a credit card. There are no other fees associated with the service and this scheme is more user-friendly than some of its competitors as it lessens the risk to the consumer and is therefore unlikely to negatively impact their credit scores.

How Splitit works at checkout (Source: Splitit)

Reimagining traditional LATAM payment methods

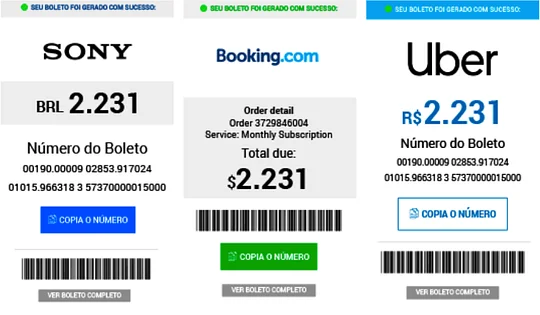

The Latin American region has a high unbanked population and is still heavily cash and credit card oriented. One payment option that is complementary to these methods and used widely across the region is vouchers with a barcode used for payment for both B2C and B2B transactions. In Brazil, they are known as Boleto Bancário, Oxxo in Mexico and Baloto in Columbia.

These vouchers have a barcode, corresponding serial number, transaction amount, issuing bank code, customer information, description and a due date by which the payment must be completed. Once presented, the consumer can either print it and pay using cash or payment cards at participating agents, or pay online using a bank transfer. The fact these vouchers can be accessed through a computer or smartphone shows adaptation to a changed environment where customers have technology at their fingertips, and their ongoing use reflects a widespread perception that they are more secure than card payments.

These factors are reflected in the parts of the region that are seeing a huge rise in e-commerce. Consumers want the convenience of making payments while still using methods they are familiar with. In light of this, newer market entrants are focusing on shifting customers from cash-based transactions to digital ones, using mobiles and processes they are already familiar with such as the voucher schemes. A reported 30 percent of e-commerce consumers in both Mexico and Brazil pay using voucher schemes.

RecargaPay

Recarga Pay has built a mobile payment system that serves every type of consumer: banked, unbanked and businesses as well. It functions as both a payment enabler and a wallet.

Mobile Boleto

Digital/mobile boletos operate via a similar mechanism to QR codes. Customers choosing to pay boletos digitally can scan the tickets’ barcodes on their phones or type associated serial numbers into their apps to trigger pull payments from their accounts. Payments via the digital version of the voucher reduce the confirmation time from the typical two or three days to just a matter of minutes or hours. This offers great convenience to consumers, especially when it comes to retail purchases, because once the payment is confirmed, the merchant will release their products.

Mobile boleto vouchers (source: DLocal)