Best In Class Digital Money Managers: the consumer perspective

Introduction

We say it a lot, because it’s true: digital banking is only 1% finished.

We understand all too well that it can be easy to forget. This is an industry that we live and breathe, and is constantly growing and shifting. We see new products and services added to our Pulse platform every week, and explored by Sarah Kocianski in her research reports. Most recently she outlined some of the numerous, exciting, new digital money management (DMM) services which are now on the market.

That said, we also fundamentally believe in staying connected to the day to day realities of ordinary customers. Consumers are trying to solve problems and achieve goals, and the question remains as to whether the next generation of financial services are actually helping them do that. To quote another colleague, Ryan Garner, “customers don’t want your bank”. It’s no longer about commodity products, it’s about building truly digital services.

With that in mind, we wanted to explore beneath the shiny surface of digital money managers to:

- Look at how consumers are managing their money today — with DMMs or via other means.

- Find out what people are trying to achieve with the services or methods that they are using.

- Work out where DMMs are currently delivering for those using them.

- Recommend where the industry should go next.

1. How consumers manage their money today

We interviewed a representative sample of over 1,000 current account holders, from across the UK and with varying levels of income in order to find out.

DMM services have exploded for sure, but our research showed that uptake is still low:

- Only 14% claim to be using any type of DMM, including app-only banks like Monzo and Starling — which don’t proactively position themselves in this space.

- Uptake is currently skewing towards more affluent, millennial consumers — 71% of DMM users we spoke to said that they were earning £40,000 or more, and 63% were millennials.

- Low uptake isn’t because of a lack of interest — 89% of UK customers say they are actively trying to manage their finances in some way.

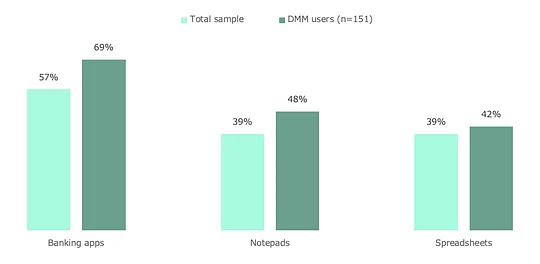

- Even though the UK is at the forefront of the fintech scene, notepads, spreadsheets and regular banking apps from incumbents are still currently carrying most of the load.

- Additionally, one in four people say that they’re only using offline tools like notepads and spreadsheets to manage their money.

Even when people have made the move to using specialist budgeting apps, they’re rarely used alone. People using specialist apps are actually more likely to use notepads to help with their financial admin.

Q5. Have you used any of the following to help you actively manage your finances in the last two years?

When we looked at groups using specific groups of tools, this is what we found:

- 26% only use offline tools like notepads and spreadsheets

- 21% only use their banking app

- 3% only use specialist budgeting apps

- 3% use only banking apps and specialist budgeting apps

It’s clear from these numbers that despite all the advances we’ve seen recently, non-digital tools continue to play an essential role in helping people manage their finances. The fact that consumers are stitching together their own systems using multiple different services and hacks shows that there are still plenty of opportunities for DMMs to offer more.

We wanted to dig further, to understand what these opportunities could be. So, in parallel to our quantitative research, we also did in-depth individual interviews with 13 (for luck!) consumers to hear about their personal money management systems and pain points with DMMs in their own words. Take a listen below.

2. What people are trying to achieve with the services that they’re using

We’ve talked before about how the best digital money managers in the market are starting to successfully leverage digital RICHES (Real-time, Intelligent, Contextual, Human, Extendable and Social).

There’s no doubt that real-time notifications, aggregation and categorisation have been a massive improvement for many consumers. These features offer support for some genuine problems in consumers’ financial lives such as trying to understand how much money they have spent and have left to spend, or trying to identify places where spending can be adjusted to pay for other things.

But whilst this is a great first step, what we see in our market analysis and heard repeatedly in our interviews is that for many users this is still just data collection. It doesn’t provide the actions, or the ‘so what’, that connects features and services to the outcomes people want to achieve.

Here’s an example of one Monzo user who still uses a spreadsheet to ‘hack’ the insights which he isn’t currently getting from the app.

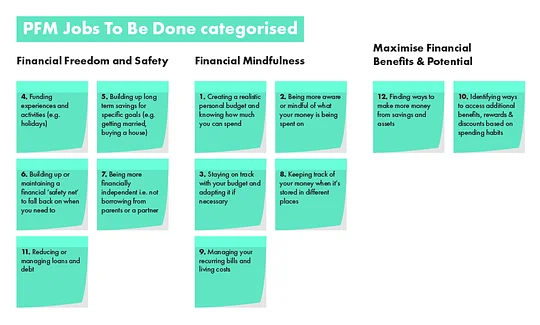

At 11:FS, we apply Jobs To Be Done theory to step away from current products and services, and help us get under the skin of what consumers are actually looking for.

Through analysing our one-on-one interviews with consumers we identified 12 core ‘jobs’ that currently influence how people attempt to manage their money.

In no particular order:

To measure the size of the opportunity these jobs present to the market we used a trade off questioning technique in an online survey. This aims to simulate how customers prioritise one job over another in real life. The trade-off questioning technique (also known as MaxDiff) asked consumers to tell us which of these jobs were the most and least important to them in their day to day lives, and which they felt were currently best and worst served by existing financial products and services.

The top three most important, when looking across all consumers were:

- Managing recurring bills and living costs.

- Building up or maintaining a financial ‘safety net’ to fall back on when needed.

- Staying on track with a budget and adapting it if necessary.

So how are consumers currently staying on top of these areas, and what’s holding them back?

Recurring Bills and Living Costs

When it comes to managing recurring bills and living costs, consumers in our panel are most likely to be relying on their online banking or bank apps (49%) to see that money is going in or out on time. For many, it’s a process which is reactive rather than anticipatory.

Routine and consistency is the paramount objective for consumers here. Key problems include bills which get more or less expensive each month, meaning it’s hard to establish a stable monthly budget, and bills that pop up as an unpleasant surprise on a quarterly or annual basis.

Financial 'safety net'

Our panel flagged this as their second most important mission with their money, but we saw numerous instances in our individual interviews of good intentions falling by the wayside. Looking at our data, we see that most people are still trying to make this happen through manual processes that take up time and rely on individual structure and motivation. In many instances, chunks of money are being physically lifted from one account to another, rather than relying on automated processes like direct debits or ‘sweep the change’ functionality. Our panel were more likely to use physical storage spaces like jars or envelopes than ‘round up’ style savings accounts to help create a buffer.

Alongside these practical challenges, consumers are also struggling first and foremost to work out where in their day-to-day budget money for a buffer could practically come from. And once people do start to find money to stash away, many admit that they find it difficult not to dip in these funds for other non-emergency things.

Staying on track with and adjusting budgets

This is another area where the online banking app currently remains king, with good old pen and paper and trusty spreadsheets in joint second place.

Within these more manual systems widespread problems persist — large unexpected costs, and bigger one-off costs (such as flights), are still difficult to fit within a monthly set up.

3. Where DMMs are currently delivering for their users

We saw earlier that DMMs are currently skewing towards a relatively affluent millennial audience, and the satisfaction levels in our research shows that for this audience they are successfully delivering against two key but interconnected areas. Firstly, managing recurring bills and living costs, and secondly, setting up a realistic budget so you know how much you can spend.

This tallied with what we heard in our one-to-one interviews. DMM users told us how account linking and automatic categorisation features enable them to easily stay on top of bills and maintain an up-to-date view of where they are.

In these two areas, DMMs are able to provide a clear return on time investment for users. They streamline time-consuming manual spend logs and budget tallying that was previously being done on a less frequent basis, often in Excel.

With these basics taken care of, the foundations are there for DMM users to start thinking more progressively and ambitiously about their finances. So, whilst it’s great to see that DMMs are already meeting some key needs for their users, we also wanted to identify where the real opportunities lie to take DMMs to the next level and develop truly best in class services.

4. Where the industry should go next

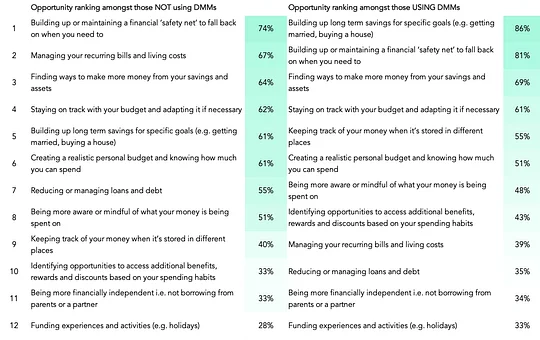

We combined the importance and satisfaction from our trade-off exercise to create an ‘opportunity’ score for each of the jobs that consumers are trying to get done. This gives us the sweet spot between what matters to consumers, and where current satisfaction levels show room for improvement.

DMMs have the same two challenges which impact most services, regardless of sector:

- Reaching more people and having a bigger impact on the sector.

- Keeping current users active and engaged.

To look at the opportunities in each of these spaces, we ran our analysis through the lens of those who aren’t already using DMMs, and those who are.

Reaching more people

Recurring bills and living costs

This ranks as the second highest opportunity area for those not currently using DMMs, and jumps up to the number one priority when we zoom in on consumers with the lowest income levels. We saw in our one-on-one interviews how critical this area was for people on tight budgets, with people often thinking weekly rather than monthly in order to stay on track.

Given how satisfied current users are in this space, this feels like something that DMMs should be heavily promoting. It’s a promise which they can take out to non-users and be confident that their current offerings will deliver on.

Reducing or managing loans and debts

Although this opportunity sits lower down the priority list, it may be something that money managers need to tackle if they aspire to become truly mainstream. After a post-recession dip, consumer credit levels have been steadily on the increase and Bank of England figures now show that individual borrowing has surpassed 2008 levels. If DMMs aspire to become a true hub for users’ financial lives, loans and debts need to be factored in.

This is particularly the case if DMMs aspire to reach out to a broader audience. When we looked at the opportunity analysis, we saw that this was a far higher priority for those with lower incomes.

Keeping current users active and engaged

Building up long term savings for specific goals

Once the basics of budgeting and bill tracking are covered off, this is becoming a greater priority for DMM users and jumps to the top of the opportunity list.

In our one-to-one interviews, DMM users talked about the satisfaction they got from being able to see beyond day to day money management and start working towards tangible goals, like big holidays or one-off purchases.

I actually enjoy the clarity. I realised that with clarity then you can plan what to do.

DMM user

I think it’s just knowing how much I can put in to savings, and almost seeing savings as a payment. So knowing that this month I’ve got to pay this amount towards a saving account. I think that’s been a big positive.

DMM user

However, our quantitative research showed that DMM users are looking for more nuanced and sophisticated guidance. Whilst non-users primarily struggle with setting money aside in the first place, DMM users were more likely to cite problems with staying on track with their savings.

Developing and refining functionality which helps users to stay motivated to save over time and understand how long it will take to reach their targets will help to keep them engaged.

Keeping track of money stored in different places

Getting the most out of your money often means distributing it across multiple different platforms and services, creating a multi-faceted system that is difficult for most consumers to stay on top of.

As our survey highlighted, many people still utilise a variety of different tools (digital or otherwise) in order to build a system that works for them. Yolt-style aggregating solutions are a great starting point for those who have discovered them, but this is an area which actually matters more to DMM users.

Our view? DMMs have opened customers’ eyes to the power of a financial control centre. It’s becoming more important to them, but they want to see a lot more. This is an area which – unlike recurring bills – DMMs have not yet ‘nailed’ and there’s still opportunity to go further.

Opportunities for both non users and users

A financial 'safety net' to fall back on

This is a universally important area where there is still loads of opportunity for digital management solutions to help consumers, regardless of whether they’re already using DMMs or not.

Many people are falling short because, as we saw earlier, they’re overly reliant on manual processes which are easily forgotten, subject to human error, or overridden by short term pressures like needing to pay an unexpected bill. For those using DMMs, the challenge is less about getting started and more about staying motivated to main their safety net over time.

This should be prime opportunity space for intelligent digital services to step up, deploying behavioural theory and nudges and open banking initiatives to help make this easier for consumers.

Finding ways to make more money from your savings and assets

UK Consumer Confidence tracking shows that consumers are currently more likely to feel like it’s better to be saving than spending, but high street savers currently offer relatively meagre rewards. The initial success of Marcus’ UK launch shows that consumers are hungry for any kind of interest rate, with 50,000 accounts opened in the first two weeks alone.

Yet research recently commissioned by Wealthify also showed that consumers appear apathetic towards existing solutions in this space, with apps optimistically downloaded but then wallowing unused on home screens. Whilst huge amounts of progress has been made, there’s evidently still something that needs to be fixed here.

Tell me ways to get the most out of my money. Like if I could invest in something, because I’ve tried investing in something before and it didn’t really go very well. And I feel like that’s because I didn’t have the knowledge about it, so probably if they could advise me on how to make more money with the money I’ve got already, rather than saving more ... just how to get the most out of what I’ve already got, rather than trying to limit myself and take away things that I want to do.

Jonathan

So what does ‘best in class’ ultimately look like for consumers?

- To get DMMs into the hands of more people, providers need to start talking more about how digital solutions help to minimise the stress of bills and living costs, particularly the less regular ones which tend to slip out of people’s mental budgets.

- DMMs need to start thinking about how they can incorporate loans and debts if they aspire to build a hub that truly reflects users’ financial systems.

- We need to talk about the safety net. Across the board, there is a stronger role for DMMs to play in helping people to take their good financial intentions and embed those into seamless or even automated behaviours that help provide the security that consumers crave but struggle to execute.

- Our results show that as DMMs empower users to have more control and oversight over their finances, they are looking to take more action and make positive changes in their lives. For existing solutions to continue to delight their customers, they need to build in more advanced savings options which kick in as consumers start to clear away the clutter.

- Helping people to feel in control of their money is one thing, but consumers still aspire, or even expect, to make money from their savings with minimal personal effort. Monzo’s move into savings pots with interest show that this is being recognised by the challengers, but anyone who can find a way to meaningfully differentiate in this space has a chance to really steal market share.