8 takeaways from our latest Banking as a Service episode

Frankie Jones

Senior Content Writer

The fourth episode of our brand-new video series, Decoding: Banking as a Service, is here! If you missed it (or any of the others) catch up here. Here’s a rundown of this episode if you prefer reading to watching 📖

The innovation required to jump on the BaaS bandwagon can feel threatening for big banks. But there are a number of benefits they can leverage from adopting BaaS - and they don’t really have a choice anymore.

What are the benefits?

- Cost cutting - Outdated legacy systems have been holding big banks back for years now, but restructuring this outdated ecosystem and rebuilding a more modern ecosystem and culture is going to take some time. Partnering with brands will enable banks to grow their balance sheets in a way they haven’t before, and take away all the cost of distributing financial products.

They’ll either have to get on the bus or be left behind.

Seth Ross, Greendot

How might the role of big banks change?

- Big banks can no longer rely on their brands to instil trust - The likes of HSBC and Barclays are renowned for being safe; the presence of big, familiar branch names on the high street gave people a sense of security. But with some banks considering closing up to 50% of their bricks and mortar stores post-pandemic, they can no longer rely on this.

- Everything is moving online - People are realising how much easier many banking services are when done online rather than in-branch. For example, over the last year, 69% of account openings in the US came via a mobile app.

At the end of the day, people might not love banks, but they trust them.

Yolande Piazza, Google Cloud

What do big techs bring to BaaS?

- It allows them to differentiate their services - Financial services offer a very attractive opportunity to grow the economic pie that they’re able to capture, helping them increase their stickiness for customers.

- They can provide speed and agility - Tech giants can help with speed and the provision of services without taking over the customer relationship. They can enable an organisation to run smoothly and efficiently, while reducing their operational costs.

Where do challenger banks fit in this ecosystem?

- They’ll become the ones pushing the boundaries of what’s possible - Challenger banks could become our ‘financial control centres’, where a number of fintech apps are aggregated in one place to provide a seamless experience.

- Big banks will become their partners - Instead of seeing traditional banks as direct competitors, challenger banks might begin to see big banks as players who can help them with the difficult back-end operations.

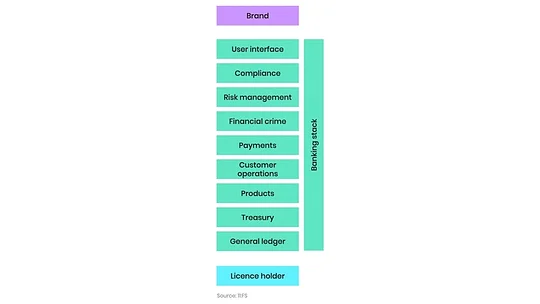

- They have the advantage of operating up and down the stack - Some players have set themselves up to work as consumer facing propositions, while others have the technical capabilities which enable them to drop further down the stack. Take Starling, for example. They’ve effectively built a bank on top of a set of APIs. Now, they’re offering themselves out as a BaaS player and a lot of people are interested.

11:FS Banking as a Service stack

They’ve had a head start because they’ve been built in that modular way that makes BaaS so much easier to engage with.

Kate Moody, 11:FS

Don’t forget to sign up for instant updates when new episodes of Decoding: Banking as a Service launch!